Wie

bereits im Artikel "Schweinezyklus" beschrieben, wird die Rohstoffindustrie der Zukunft weiterhin die wiederkehrende Gewohnheit zeigen, einen Boom durch eine Überversorgung abzulösen.

In der

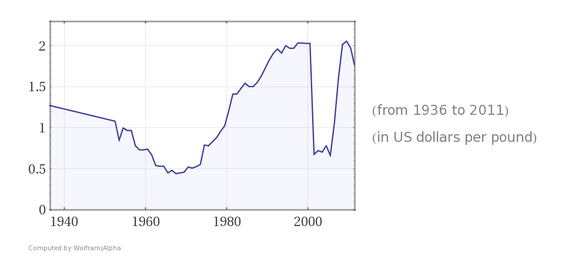

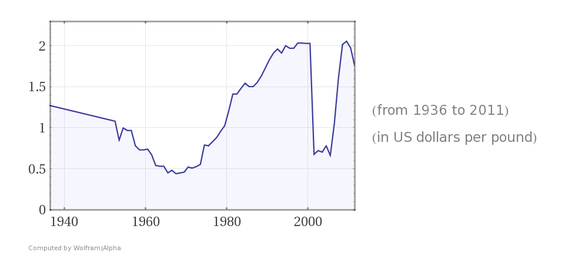

Vergangenheit stiegen die Preise für Lithium, eines der seltensten Elemente auf der Erde, welches in wiederaufladbaren Batterien verwendet wird, wobei die boomende

Nachfrage insbesondere durch das weltweite Wachstum im

Sektor Elektromobilität getrieben wurde. Dabei steigt die Fördermenge kontinuierlich, nicht zuletzt dank der schnellen, aggressiven Expansionspläne von Elon Musks Tesla Motors

Inc.

Aktuell kontrollieren die vier größten Lithium

Produzenten Rockwood Holdings Inc., Soc. Quimica & Minera de Chile SA, Albermarle Corp. und FMC Corp. ca. 90

Prozent des Marktes. Durch die

steigenden Preise werden diese Unternehmen versuchen, ihre Produktion zu steigern, während eine Vielzahl von Newcomern ebenfalls in die Produktion von Lithium einsteigen werden.

Aktuell haben die größten Vier selbst bei steigenden Preisen

unterhalb der maximalen Kapazität produziert. So entfielen bei FMC im vergangenen Jahr nur 7,3 Prozent des Umsatzes auf

Lithium, der Rest wurde mit Chemikalien für Landwirtschaft, Gesundheit und Ernährung erwirtschaftet. Sollten jedoch weitere Wettbewerber in das Feld einsteigen, so werden die großen Vier gezwungen sein, die Produktion zu

erweitern, um ihre Marktanteile zu schützen. So wird sich laut FMC der bis

2020 erwartete Umsatz von Lithium im Vergleich zu 2016 verdoppeln, was einem Umsatzzuwachs von 25%

p.a. entspräche.

Ein Rückgang der Nachfrage ist dabei nicht abzusehen.

So plant Tesla ab 2017 mit dem Verkauf seiner Modell 3-Limousine zu beginnen. Dazu wird die Prokduktion in der riesigen Batterie-Fabrik "Gigafactory" in Nevada beginnen. CEO Elon Musk begann mit

dem Bau der 5 Milliarden US-Dollar teueren Anlage, mit dem Ziel, bis 2018

500.000 Elektroautos zu produzieren. Die Anlage ist ein Joint-Venture zwischen Musks Firma Tesla und dem Batteriehersteller Panasonic.

Während Lithium nur 2 Prozent des in den Tesla-Batterien eingesetzten Materials ausmacht und von Musk als "nur das Salz auf dem Salat" bezeichnet wurde, bewirkt die e-Mobilität trotzdem eine

signifikante Nachfrageveränderung für den Lithiummarkt. So schätzt Goldman Sachs den

Materialbedarf an Lithium für eine Tesla Modell S Batterie auf 63 Kilogramm (139 Pfund), verglichen damit sind die 5 Gramm, welche für ein Mobiltelefon benötigt werden, verschwindend

gering.

So ist es nicht verwunderlich, dass sich die

Nachfrage nach Lithium weltweit von 2016 bis 2020 verdoppeln wird.

Wenn der Verbrauch derart wächst, wird der Markt laut Benchmark Minerals Intelligence Ltd. eine zusätzliche Jahreskapazität von 100.000 Tonnen benötigen um den Bedarf zu decken.

Etwas mehr als die Hälfte des

zusätzlichen Outputs wird dabei wahrscheinlich von den bestehenden Herstellern stammen. Dies führt dazu, dass die Förderung von Lithium auch für neue Marktteilnehmer rentabel wird.

Insbesondere die Fördermengen Chiles und Australiens wurden bereits auf die gestiegene Nachfrage ausgerichtet.

Interessierte Anleger sollten jedoch langfristig zwei wesentliche Gesichtspunkte nicht unberücksichtigt lassen: Lithium ist endlich und ein Anziehen des Preises wird langfristig ein realistisches Szenario werden. Aus diesem Grund könnte es durch die Entwicklung von Brennstoffzellenantrieben oder durch die Entwicklung von Batteriezellen, welche nicht auf das Element Lithium angewiesen sind langfristig zu einer Substitution von Lithium Batteriezellen kommen. So entwickelt aktuell Belenos, ein Tochterunternehmen der Swatch Group eine Batterie, welche auf Vanadium statt auf Lithium basiert. Dies könnte sich zu einem Paukenschlag für die Automobilindustrie entwickeln.

Lithium - the Fuel of Electromobility

As already described in the article "Pork Cycle," the extractive industry of the future will continue to show the recurring habit of oversupplying as a means of superseding a boom.

In the past, prices for lithium, one of the rarest elements on earth, used in rechargeable batteries, rose and the boom in demand was driven by the global growth in the sector of electromobility. At the same time, output is increasing continuously, not least due to the fast, aggressive expansion plans of Elon Musk's Tesla Motors Inc.

Currently, the four largest lithium producers Rockwood Holdings Inc., Soc. Química & Minera de Chile SA, Albermarle Corp. and FMC Corp. are controlling about 90 per cent of the market. Due to the increasing prices, these companies are going to try to increase their output while a multitude of newcomers are going to join the production of lithium as well.

So far, the big four have been producing below maximum capacity even with rising prices. For instance, FMC generated only 7.3 per cent of its revenue from lithium last year, the rest coming from chemicals used in agriculture, health and nutrition. Should other competitors join the field however, the big four will be forced to expand their output in order to protect their market share. According to FMC, its expected revenue from lithium up until 2020 will double in comparison to 2016 which would correspond to a 25% increase in revenue p.a.

At the same time, demand for lithium remains stable. Tesla plans to start the sale of its Model 3 sedan from 2017 on. Also, production will begin in the battery plant "gigafactory" in Nevada. CEO Elon Musk started the construction of the $5 billion investment with the goal of producing 500,000 electric cars by 2018. The investment is a joint venture by Musk's company Tesla and Panasonic, the battery manufacturer.

While lithium makes up only 2 per cent of the material used in the Tesla batteries, and was only described by Musk as "just the salt on the salad," electromobility still represents a significant shift in demand for the lithium market. Goldman Sachs estimates the amount of lithium required for a Tesla Model S battery to be 63 kilogram (139 pounds); compared to that, the 5 gram that are needed for a mobile phone are incredibly small.

Thus, it is not surprising that the demand for lithium will double globally between 2016 and 2020. According to Benchmark Minerals Intelligence Ltd., an additional annual capacity of 100,000 tons will be required to cover demand if consumption grows like that. Just more than the half of the additional output would probably come from the established producers. This leads to the support of lithium becoming economic also for new market participants. Especially the output of Chile and Australia have already been adjusted to the increased demand.

Interested investors should, however, take into account two crucial aspects in the long-term: Lithium is finite and an increase in its price will become a realistic scenario in the long-term. Therefore, the development of fuel cells or battery cells that are not dependant on the element lithium might become substitutes for lithium battery cells. Currently, Belenos, a subsidiary of the Swatch Group, is developing a battery that is based on vanadium instead of lithium. This could become a real thunderbolt for the automotive industry.

Kommentar schreiben