Albert Einstein wird folgendes Zitat zugeschrieben:

„Die größte Erfindung des menschlichen Geistes? – Die Zinseszinsen!“

Eines der mächtigsten Hilfsmittel beim langfristigen Vermögensaufbau ist das Verständnis um den Effekt des Zinseszinses, welches wir euch in diesem Artikel näherbringen möchten. Die wichtigste Botschaft, die wir hier vermitteln möchten, ist die Erkenntnis, wie immens wichtig die Nutzung des Zinseszinseffektes für einen langfristigen und nachhaltigen Vermögensaufbau ist.

Der Zinseszinseffekt

Einfach ausgedrückt ist der Zinseszinseffekt der zeitlich kumulative Vermögenszuwachs, welcher sich durch die Anlage eines festen Betrages ergibt, wobei der Zinsertrag des ursprünglich investierten Betrags mit dem gleichen Zinssatz reinvestiert wird.

Zunächst einmal die langweiligen Fakten:

Berechnet wird das Endkapital nach folgender Formel:

KE = KA * ((p / 100) + 1)n

KE: Endkapital inkl. Zinsen nach n Jahren

KA: angelegtes Anfangskapital

p: Zinssatz in Prozent

n: Anzahl der veranschlagten Jahre.

Es ist somit ersichtlich, dass diese Formel für den Anleger genau drei Dinge bedeutet:

1. p sollte so groß wie möglich sein, allerdings bei überschaubarem Risiko,

2. n sollte so groß wie möglich sein (Stichwort Sport und gesunde Ernährung :-)

3. Das Vorzeichen vor KA sollte unbedingt positiv sein.

Man muss dabei darüber im Klaren sein, dass n für alle Sterblichen endlich ist. Bevor wir in philosophische Gedanken abgleiten, hier ein (zugegebenermaßen unrealistisches, aber anschauliches) Beispiel:

Sie legen im zarten Alter von 15 Jahren 1000 Euro an, um für ihre Rente mit 70 Jahren (weniger unrealistisch) vorzusorgen. Welcher Auszahlungsbetrag ergibt sich innerhalb dieser 55 Jahre, wenn man einen Zinssatz von 6% zugrunde legt? Die Antwort ist: 24.650,32 Euro. Bei der Berechnung sind Inflation sowie Steuern und Gebühren nicht berücksichtigt. So werden aus 1000 Euro über einen Zeitraum von 55 Jahren 24.650 Euro.

Um sich den Einfluss des Faktors Zeit nun zu veranschaulichen: Wie viel müsste nun jemand anlegen, der sich mit 30 Jahren erst dazu entschließt, im Alter einen identischen Betrag zur Verfügung zu haben? Die Antwort ist 2.396,56 Euro, also mehr als das Doppelte.

Vorsicht ist allerdings geboten: Diese Formel funktioniert identisch, wenn das Vorzeichen vor KA negativ ist, man also Schulden macht. Erfahrungsgemäß ist dann auch p naturgemäß deutlich größer (Stichwort Dispo- bzw. Überziehungszins), weshalb man für einen erfolgreichen Vermögensaufbau immer darauf achten sollte, frühzeitig seine Schulden abzubauen.

Anbei einige Diagramme, die den Einfluss des Startkapitals und der Verzinsung sehr schön verdeutlichen:

Wie immer gilt auch hier: Versuch macht klug, probieren Sie einfach einmal verschiedene Konstellationen mit unserem Zinseszinsrechner, dann wird schnell klar, was es mit n und p auf sich hat. Da wir n außer durch Apelle, früh mit dem Sparen zu beginnen, nicht beeinflussen können, werden wir uns in diesem Blog im Wesentlichen auf das passive und aktive Management von p - dem Zinssatz - konzentrieren.

The Compound Interest Effect

Albert Einstein is accredited with the following quote:

"The greatest invention in human history? - Compound interest!"

One of the most powerful tools for long-term wealth building is the comprehension of the compound interest effect, which we want to give you an understanding of in this article. The important message that we want to convey is the comprehension of how immensely important the use of the compound interest effect is for long-term and sustainable wealth building.

The Compound Interest Effect

Simply put, the compound interest effect is the temporally cumulative capital gain, which arises from the investment of a fixed amount, whereby the interest earned from the originally invested amount is being reinvested at the same interest rate.

First, the boring facts:

The final capital is calculated using the following formula:

KE = KA * ((p / 100) +

1)n

KE: final capital including interest after n years

KA: invested initial capital

p: interest rate in percent

n: number of estimated years.

It is therefore obvious that this formula means three things for the investor:

1. p should be as large as possible, however with negligible risk,

2. n should be as large as possible (keyword sports and healthy nutrition :-)

3. The sign in front of KA should be positive at all costs.

One has to be clear about the fact that n is finite for all mortals. Before we drift off into philosophical thoughts, here is an (admittedly unrealistic, but descriptive) example:

You invest 1,000 euros at the tender age of 15, in order to provide for your pension at 70 years (less unrealistic). Which amount will be paid out after these 55 years, based on an interest rate of 6%? The answer is: 24,650.32 euros. The calculation does not consider inflation, as well as taxes and fees. That way, 1,000 euros become 24,650 euros, over a period of 55 years.

Now, to illustrate the influence of the factor time: How much would someone have to invest, when they only begin to invest at the age of 30, with the goal to have the same amount of money at hand? The answer is 2,396.56 euros, which is more than double the amount.

Caution is however required: This formula works identically when the sign in front of KA is negative, in other words, when one is incurring debt. Based on experience, p is, in that case, naturally far greater (keyword overdraft facility or overdraft interest), which is the reason why one should always make sure that their debts are repaid in a timely manner for successful wealth building.

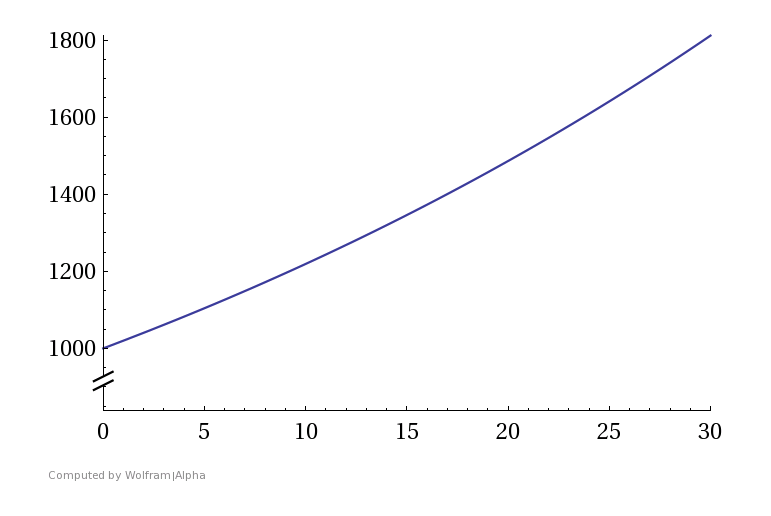

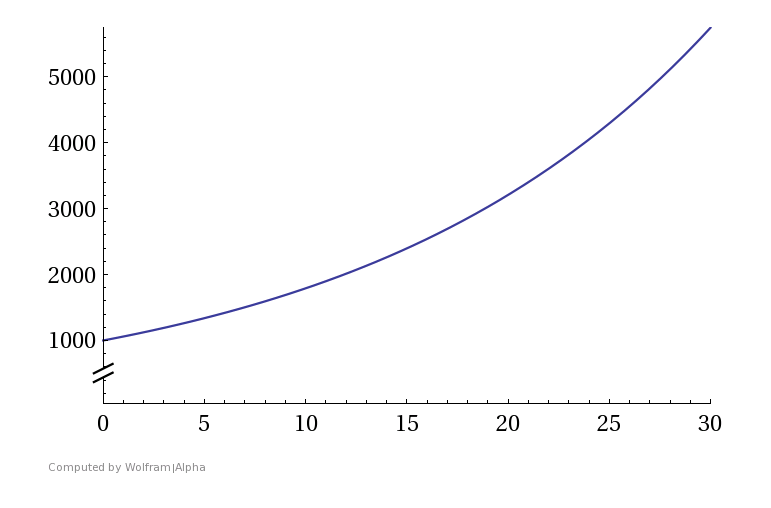

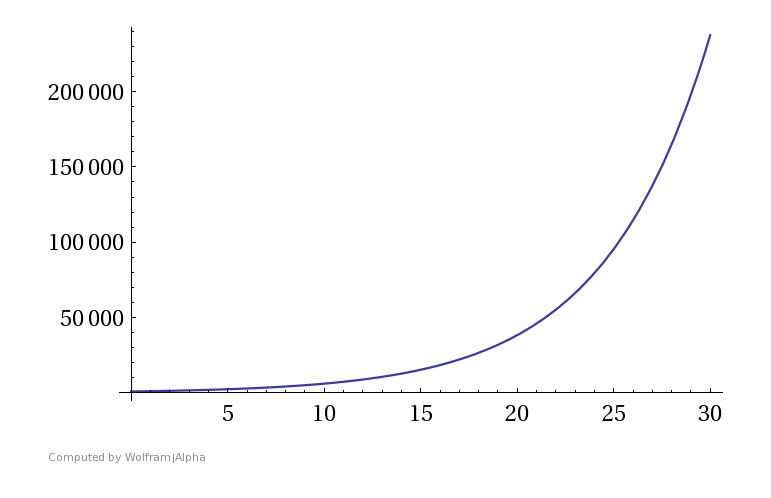

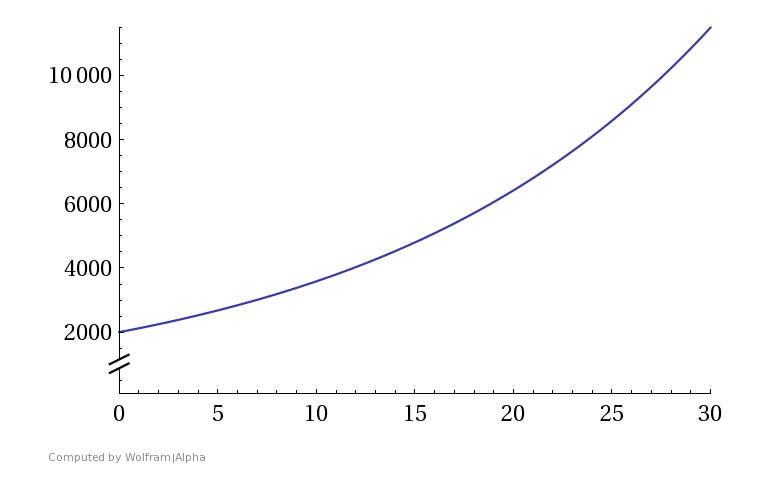

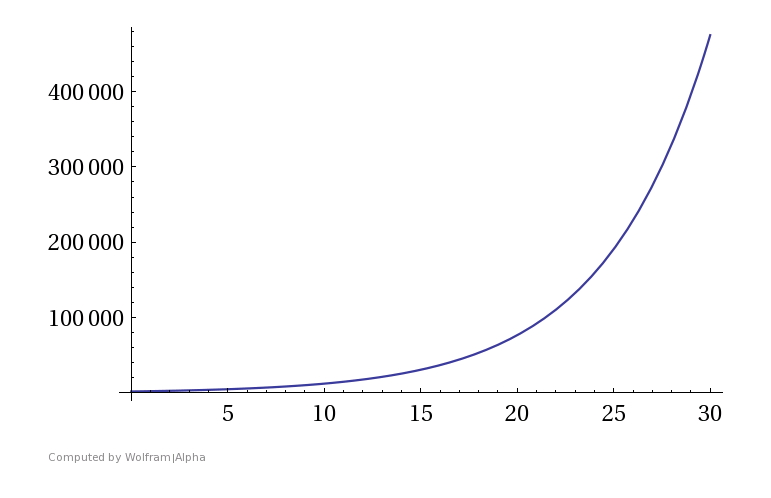

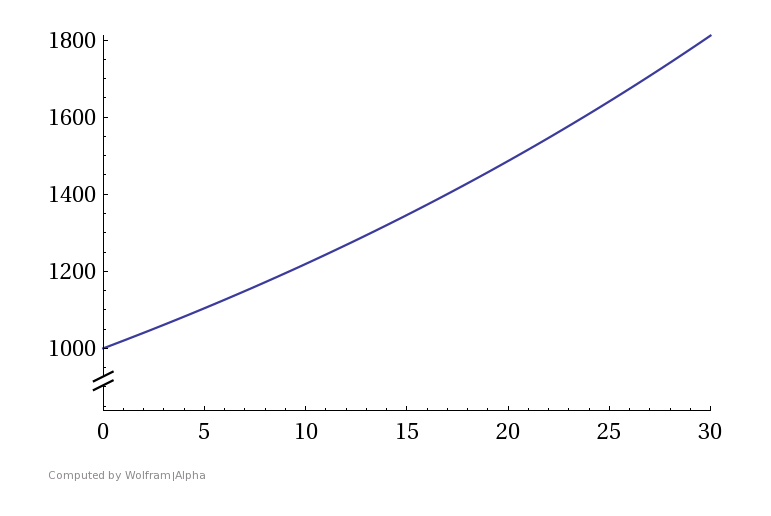

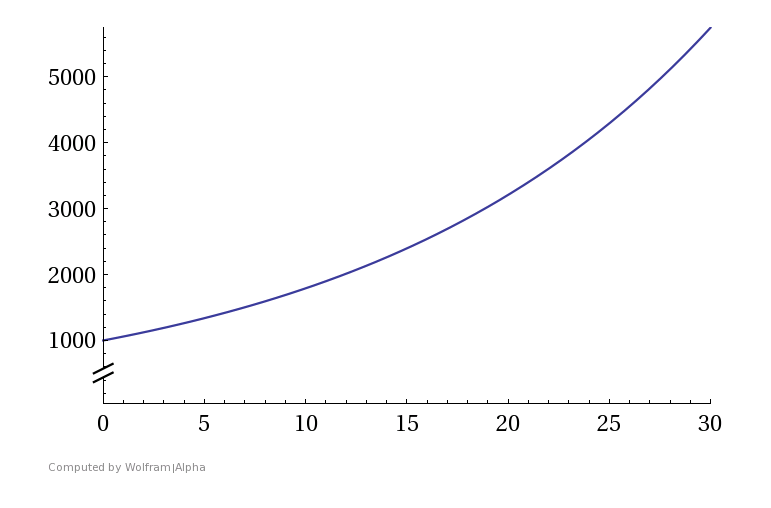

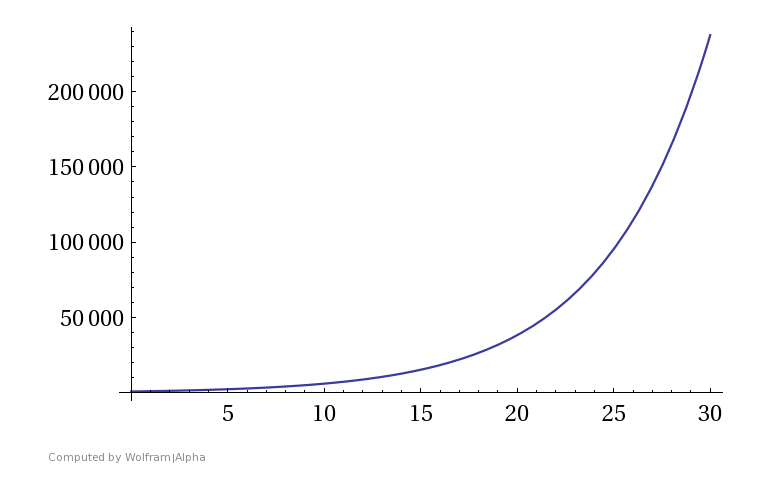

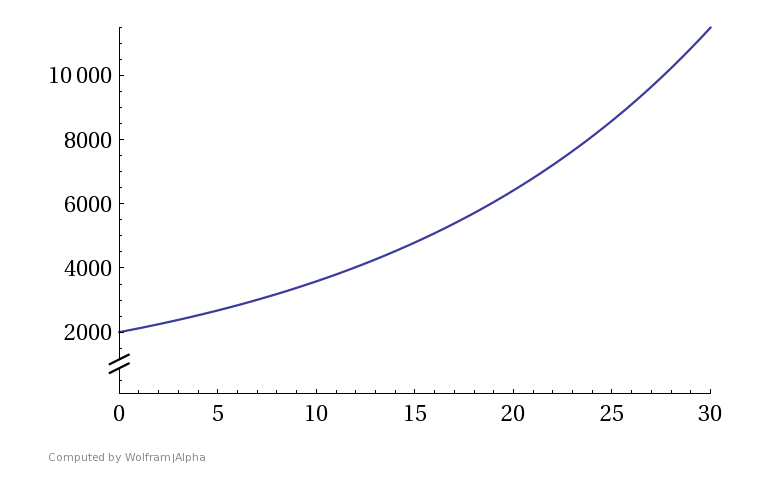

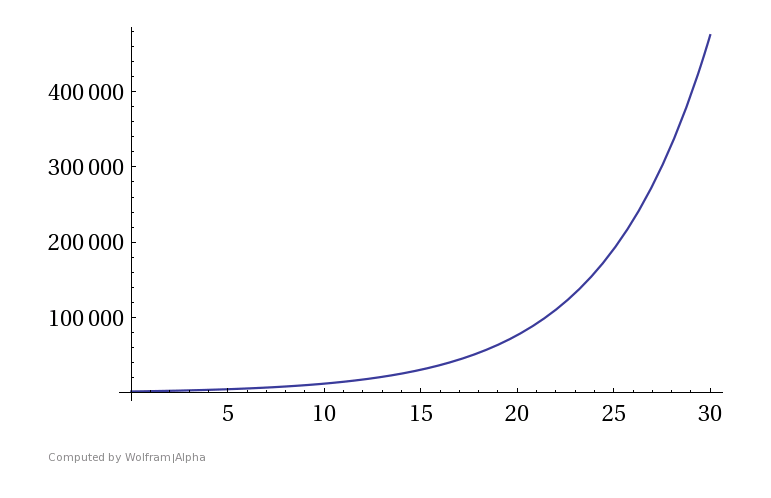

Attached are several graphs, which nicely illustrate the influence of the initial capital and the interest:

Capital gain through the compound interest effect with an initial capital of 1,000 euros and an interest rate of 2%

Capital gain through the compound interest effect with an initial capital of 1,000 euros and an interest rate of 6%

Capital gain through the compound interest effect with an initial capital of 1,000 euros and an interest rate of 20%

Capital gain through the compound interest effect after 30 years with an initial capital of 2,000 euros and an interest rate of 6%

Capital gain through the compound interest effect with an initial capital of 2,000 euros and an interest rate of 20%

As it always has, it also applies here: Nothing ventured, nothing gained. Just try out different constellations with our compound interest calculator, then it will quickly become clear what n and p are. As we cannot really influence n, except through the plea to start saving earlier, in this blog, we will mainly concentrate on the passive and active management of p - the interest rate.

Kommentar schreiben

Hobert Brundige (Donnerstag, 02 Februar 2017 10:07)

My coder is trying to convince me to move to .net from PHP. I have always disliked the idea because of the costs. But he's tryiong none the less. I've been using WordPress on numerous websites for about a year and am concerned about switching to another platform. I have heard excellent things about blogengine.net. Is there a way I can import all my wordpress content into it? Any help would be greatly appreciated!

www.smartmoneyblog.de (Samstag, 04 Februar 2017 20:09)

Dear Hobert,

I am sorry for not being able to help you with your problem, since I do not use WordPress, either blogengine.net.

Greetings

Your SMB-Team

Fae Brune (Samstag, 04 Februar 2017 21:37)

Excellent way of describing, and pleasant article to obtain data regarding my presentation focus, which i am going to deliver in college.

SMB-Team (Samstag, 04 Februar 2017 22:17)

Happy you like it! All the best for your presentation :-)

Greetings

SMB-Team

Theola Bower (Sonntag, 05 Februar 2017 15:33)

Hi would you mind sharing which blog platform you're working with? I'm going to start my own blog soon but I'm having a hard time choosing between BlogEngine/Wordpress/B2evolution and Drupal. The reason I ask is because your design seems different then most blogs and I'm looking for something unique. P.S Apologies for being off-topic but I had to ask!

SMB-Team (Sonntag, 05 Februar 2017 16:24)

Hi Theola,

I am currently using Jimdo, a German provider of web-solutions.

Adela Wynter (Montag, 06 Februar 2017 17:48)

Pretty! This was an extremely wonderful article. Thank you for supplying this information.

Dovie Hansel (Dienstag, 07 Februar 2017 02:33)

This paragraph is in fact a fastidious one it helps new the web people, who are wishing in favor of blogging.

SMB-Team (Dienstag, 07 Februar 2017 15:10)

@ Dovie @Adela,

Thanks for the comments, glad you like it :-)

Denyse Olsen (Mittwoch, 08 Februar 2017 20:14)

Hi there! This is kind of off topic but I need some help from an established blog. Is it very difficult to set up your own blog? I'm not very techincal but I can figure things out pretty quick. I'm thinking about creating my own but I'm not sure where to start. Do you have any points or suggestions? Thank you

Darla Lones (Donnerstag, 09 Februar 2017 18:35)

Howdy! This article couldn't be written much better! Looking through this article reminds me of my previous roommate! He constantly kept talking about this. I'll forward this post to him. Fairly certain he will have a great read. Thanks for sharing!